Analysis of Latest Tungsten Market from Chinatungsten Online

Domestic tungsten prices trended downwards overall this week, with the rate of decline gradually slowing, but trading volume remained low. Industry insiders believe that as the market bubble bursts and panic selling pressure decreases, the tungsten market is expected to enter a phase of stabilization and recovery. The future market will depend on the actual supply and demand dynamics of negotiations.

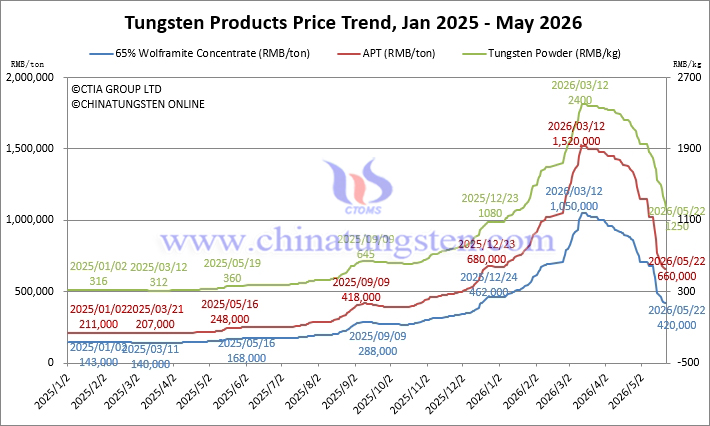

Tungsten concentrate prices fell by approximately 14.3% this week, a decrease of nearly 14 percentage points compared to the previous week, showing initial signs of stabilization near the psychological threshold of 400,000/ton. However, cautious downstream purchasing and slow market sales continue to suppress price movements.

65% wolframite concentrate was priced at RMB 420,000/ton, down 60.0% from its high and 8.7% from the beginning of the year.

65% scheelite concentrate was priced at RMB 419,000/ton, down 60.1% from its high and 8.7% from the beginning of the year.

Ammonium paratungstate (APT) prices fluctuated in line with cost trends and were influenced by long-term contracts with major tungsten producers, remaining within a narrow range of 600,000/ton. Market sentiment was cautious, and weak demand had not yet reversed.

Domestic APT was priced at RMB 660,000/ton, down 56.6% from their high and 1.5% from the beginning of the year.

European APT was priced at USD 3,000-3,280/mtu (equivalent to RMB 1.805-1.974 million /ton), up 241.3% from the beginning of the year.

Tungsten powder market saw accelerated price declines this week, falling approximately 19% week-on-week. This was mainly due to the relatively high current price of tungsten powder compared to previous levels of comparable raw material costs, leading to insufficient consumer demand and dragging down market performance.

Tungsten powder was priced at RMB 1,250/kg, down 47.9% from their high and up 15.7% from the beginning of the year.

Tungsten carbide powder was priced at RMB 1200/kg, down 48.7% from their high, but up 15.4% from the beginning of the year.

Cobalt powder prices were slightly weaker. Although raw material sources remained subject to policy controls in major producing countries, pressure on demand from cemented carbide and other consumer sectors suppressed market transactions and market sentiment.

Cobalt powder was priced at RMB 565/kg, down 2.6% from their high, but up 8.7% from the beginning of the year.

Ferrotungsten remained in a stalemate, trending downwards. Cost fluctuations were not yet stable, and steel mills showed limited purchasing enthusiasm, resulting in sluggish overall market transactions and a strong wait-and-see attitude.

70% ferrotungsten was priced at RMB 740,000/ton, down 47.9% from its high, but up 13.9% from the beginning of the year.

European ferrotungsten was priced at USD 260-270/kg W (equivalent to RMB 1.238-1.285 million /ton), down 18.5% from their high, but up 92.7% from the beginning of the year.

Tungsten waste and scrap prices have stabilized near their levels at the beginning of the year, with both buyers and sellers remaining in a wait-and-see mode, unwilling to offer excessive discounts, resulting in a narrow range of price fluctuations.

Scrap tungsten rods were priced at RMB 630/kg, down 54.0% from its peak, but up 5.0% from the beginning of the year.

Scrap tungsten drill bits were priced at RMB 580/kg, down 57.7% from its peak, and unchanged from the beginning of the year.

Prices of Tungsten Products on May 22, 2026

Tungsten Price Trend from January 2025 to May 2026