Analysis of Latest Tungsten Market from Chinatungsten Online

Tungsten prices continued their decline as cautious and shrinking demand struggled to absorb profit-taking pressure from the supply side, leading to a generally bearish market sentiment. However, as prices gradually corrected and short-selling pressure weakened, the downside potential narrowed.

In the tungsten concentrate market, the premium bubble in market sentiment was significantly reduced, easing panic selling pressure and narrowing price spreads. A bottoming-out mentality increased, but a substantial recovery still awaits positive signals from the demand side or proactive supply reductions.

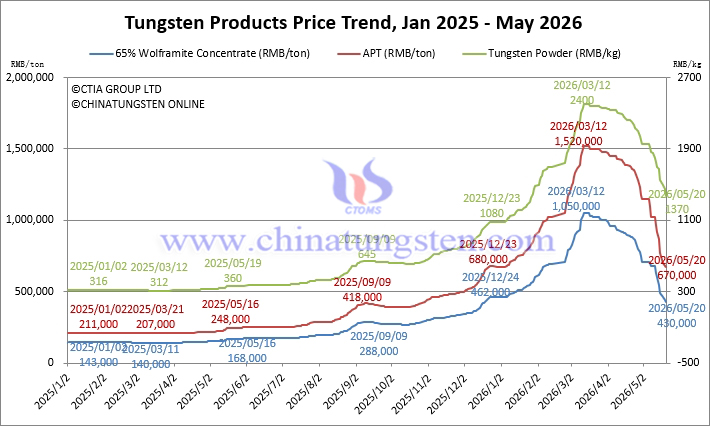

65% wolframite concentrate was priced at RMB 430,000/ton, down 59.1% from its high and 6.5% from the beginning of the year.

65% scheelite concentrate was priced at RMB 429,000/ton, down 59.1% from its high and 6.5% from the beginning of the year.

A mining company in Yunnan province auctioned off approximately 250 tons of tungsten-tin crude concentrate (4.19% WO?, 2.03% Sn) at a final transaction price of RMB 366,000/ton of tungsten and RMB 294,600/ton of tin.

In the ammonium paratungstate (APT) market, domestic prices continued to be constrained by cost pressures and weak demand, resulting in weak market liquidity. Participants were largely observing the performance of long-term contract quotations from major tungsten producers in the second half of the month. Due to differences in supply chain gaps and differing expectations, the price difference between domestic and international APT widened. The export window has temporarily opened, but actual transactions still depend on policy constraints and the realization of demand.

Domestic APT was priced at RMB 670,000/ton, a 55.9% decrease from its high, remaining flat compared to the beginning of the year.

European APT was priced at USD 3,000-3,280/mtu (equivalent to RMB 1.809-1.978 million/ton), a 241.3% increase compared to the beginning of the year.

In the tungsten powder market, prices followed the adjustment of upstream raw material prices, showing a clear downward trend. Meanwhile, weak demand from downstream sectors such as cemented carbide led to a sluggish market atmosphere and few new orders.

Tungsten powder was priced at RMB 1370/kg, down 42.9% from its peak, but up 26.9% from the beginning of the year.

Tungsten carbide powder was priced at RMB 1300/kg, down 44.4% from its peak, but up 25.0% from the beginning of the year.

Cobalt powder was priced at RMB 570/kg, down 2.6% from its peak, but up 8.7% from the beginning of the year.

In the ferrotungsten market, following the weakness of upstream raw material prices, market activity was poor, with cautious and stagnant transactions.

70% ferrotungsten was priced at RMB 780,000/ton, down 45.1% from its peak, but up 20.0% from the beginning of the year.

European ferrotungsten was priced at USD 265-275/kg W (equivalent to RMB 1.264-1.312 million/ton), down 14.6% from their high, but up 96.4% from the beginning of the year.

In the tungsten scrap market, a sluggish raw material market dominated the recent weak and volatile trend. Merchants who stockpiled at high prices this year are facing significant pressure; some are selling to cut losses, while others are unwilling to accept losses at lower prices, resulting in an overall stalemate and pressured market.

Scrap tungsten rods were priced at RMB 630/kg, down 54.0% from their high, but up 5.0% from the beginning of the year.

Scrap tungsten drill bits were priced at RMB 580/kg, down 57.7% from their high, unchanged from the beginning of the year.

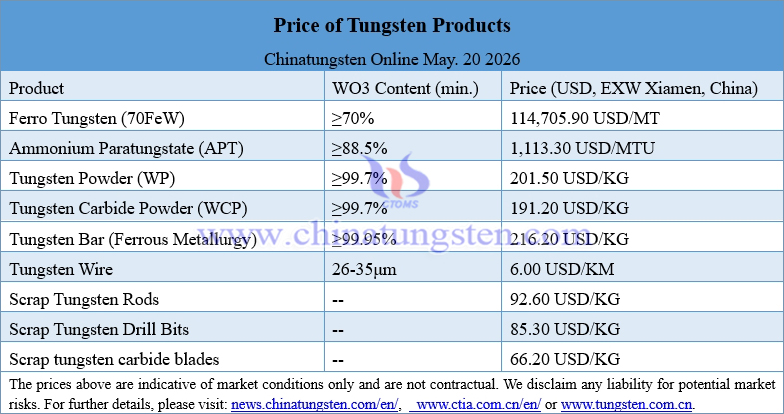

Prices of Tungsten Products on May 20, 2026

Tungsten Price Trend from January 2025 to May 2026