Analysis of Latest Tungsten Market from Chinatungsten Online

Following the May Day holiday, the domestic tungsten market failed to show signs of recovery, continuing its pre-holiday downward trend. Buyers and sellers remained locked in a tug-of-war, resulting in a relatively quiet trading atmosphere. This week, industry institutions and large tungsten companies in Jiangxi province released their price quotations, showing a significant downward shift, but these still differed from actual market prices, indicating a divergence in market sentiment.

On the supply side, the first batch of tungsten mining quotas for 2026 is 60,000 tons, an increase of 2,000 tons year-on-year. However, given the strengthened compliance measures in mining and stricter controls on trade, the overall supply environment for tungsten raw materials has not fundamentally eased. Nevertheless, the concentrated release of profit-taking, coupled with the replenishment of imported resources and scrap tungsten, has increased the market's temporary supply pressure, resulting in a relatively looser supply of circulating resources compared to the previous period.

On the demand side, market expectations for high-tech applications and strategic reserves remain positive. However, the previous high prices have had a significant suppressive effect, and currently, with prices declining, a "no-buy" sentiment prevails, leading to cautious and slow downstream purchasing activity and low restocking willingness. With weakening non-consumer demand, short-term demand-side support is relatively weak.

China Tungsten Online believes that profit-taking after the previous surge has not been fully digested, and the reshaping of downstream consumer sentiment depends on prices finding a bottom and stabilizing. In the absence of a substantial recovery in demand, tungsten prices are expected to remain in a weak and volatile cycle in the short term.

As of press time,

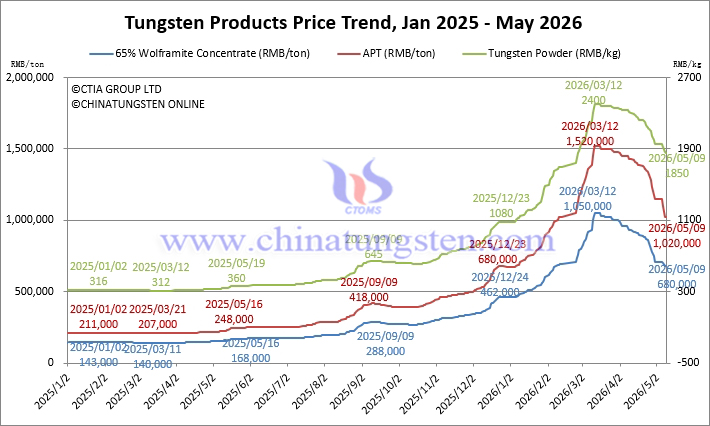

65% wolframite concentrate is priced at RMB 680,000/ton, down 35.2% from its high, but up 47.8% from the beginning of the year.

65% scheelite concentrate is priced at RMB 679,000/ton, down 35.3% from its high, but up 47.9% from the beginning of the year.

Ammonium paratungstate (APT) is priced at RMB 1,020,000/ton, down 32.9% from its peak, but up 52.2% from the beginning of the year.

European APT is priced at USD 3,000-3,280/mtu (equivalent to RMB 1.807-1.976 million/ton), up 241.3% from the beginning of the year.

Tungsten powder is priced at RMB 1,850/kg, down 22.9% from its peak, but up 71.3% from the beginning of the year.

Tungsten carbide powder is priced at RMB 1,780/kg, down 23.9% from its peak, but up 71.2% from the beginning of the year.

Cobalt powder is priced at RMB 575/kg, down 0.9% from its peak, but up 10.6% from the beginning of the year.

70% ferrotungsten is priced at RMB 1,030,000/ton, down 27.5% from its peak, but up 58.5% from the beginning of the year.

European ferrotungsten is priced at USD 270-298/kg W (equivalent to RMB 1.287-1.42 million/ton), down 12.6% from their peak but up 106.6% since the beginning of the year.

Scrap tungsten rods are priced at RMB 680/kg, down 50.4% from their peak but up 13.3% since the beginning of the year.

Scrap tungsten drill bits are priced at RMB 630/kg, down 54.0% from their peak but up 8.6% since the beginning of the year.

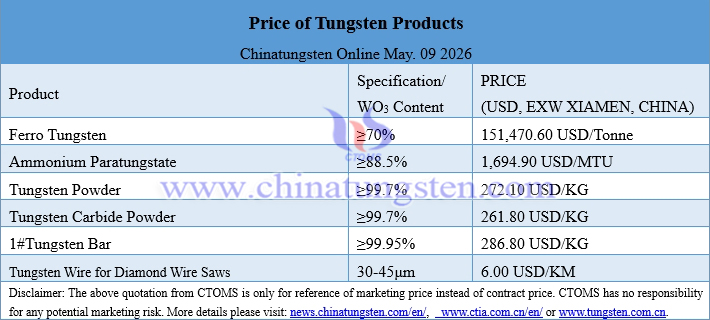

Prices of Tungsten Products on May 09, 2026

Tungsten Price Trend from January 2025 to May 2026