Analysis of Latest Tungsten Market from Chinatungsten Online

Tungsten prices declined this week, mainly due to factors such as increased profit-taking in the raw material sector, cautious purchasing by downstream end-users, and a new round of price reductions in long-term contracts from major tungsten producers.

The previous price surge in tungsten led to substantial profits for some miners and traders, resulting in a significantly increased willingness to realize gains. Some speculative positions held earlier are facing financial pressure and have had to actively deleverage to control risk. Currently, the price trend is showing a decline from its high point, leading to insufficient purchasing activity from downstream users.

However, the scarcity of tungsten resources and its strategic premium continue to support the market. According to China Tungsten Online, as historical inventories are gradually depleted, alloy and downstream sectors are releasing restocking demand. Furthermore, the inverted price structure between domestic and international tungsten markets has reversed, with some overseas demand returning.

Based on the current supply and demand fundamentals and macroeconomic expectations, China Tungsten Online believes that a bearish sentiment will continue to dominate the market in the short term, with tungsten product prices in a downward trend. However, the overall decline is relatively rational and restrained, and a significant correction below the beginning-of-the-year price level is unlikely. It is worth noting that the trading structure of the tungsten scrap market differs significantly from that of the virgin tungsten market. Participant concentration is lower, retail investor sentiment is more easily swayed, and market volatility risk is relatively higher.

As of press time:

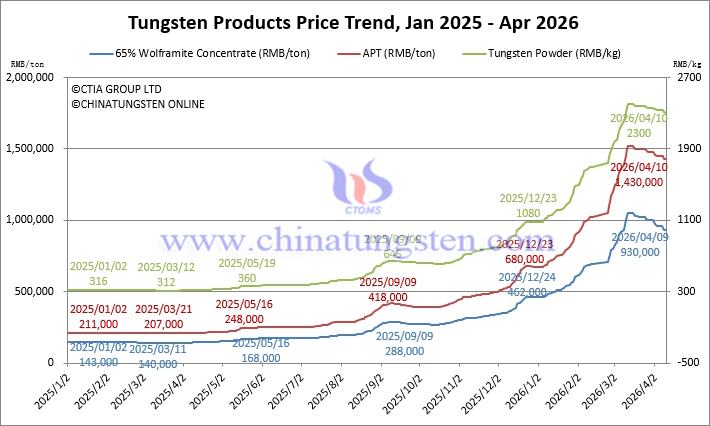

65% wolframite concentrate is priced at RMB 930,000/standard ton, down 3.1% week-on-week, but up 102.2% year-to-date.

65% scheelite concentrate is priced at RMB 929,000/standard ton, down 3.1% week-on-week, but up 102.4% year-to-date.

Ammonium paratungstate (APT) is priced at RMB 1,430,000/ton, down 1.4% week-on-week, but up 113.4% year-to-date.

European APT is priced at USD 2,800-$3,190/mtu (equivalent to RMB 1,693,000-1,929,000/ton), up 0.7% week-on-week, but up 225.5% year-to-date.

Tungsten powder is priced at RMB 2,300/kg, down 1.7% week-on-week, but up 113.0% year-to-date. Tungsten carbide powder is priced at RMB 2240/kg, down 1.8% week-on-week, up 115.4% year-on-year.

Cobalt powder is priced at RMB 580/kg, unchanged week-on-week, up 11.5% year-on-year.

70% ferrotungsten is priced at RMB 1.33 million/ton, down 3.6% week-on-week, up 104.6% year-on-year.

European ferrotungsten is priced at USD 310-330/kg W (equivalent to 1.483-1.579 million/ton), unchanged week-on-week, up 132.7% year-on-year.

Scrap tungsten rods are priced at RMB 980/kg, down 4.9% week-on-week, up 63.3% year-on-year.

Scrap tungsten drill bits are priced at RMB 960/kg, down 4.0% week-on-week, up 65.5% year-on-year.

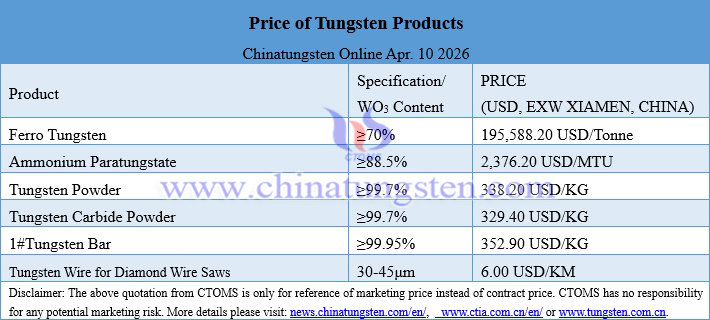

Prices of Tungsten Products on April 10, 2026

Tungsten Price Trend from January 2025 to April 2026